Background

Special Drawing Rights (SDR)What exactly are SDR?

SDR is an instrument created by the IMF in 1969 for a problem that existed with the Bretton Woods fixed exchange system. At the time, central banks of each country had to hold reserves in US dollar or gold to maintain their fixed exchange rates, but there was not enough US dollars and gold to serve this purpose. SDR would serve as an international reserve asset (worth 1 US dollar or 0.888671 grams of gold) to supplement foreign reserves, but the Bretton Woods system collapsed in 1973.

In the modern era, SDR serve primarily as a unit of account for the IMF. SDR served as a liquidity instrument during the 2008 Global Financial Crisis. Only SDR 21.4 billion existed until the financial crisis and then the IMF created SDR 161.2 billion in August 2009 so that countries could supplement their foreign reserves by borrowing SDR from other IMF members. SDR 204.1 billion exist today.

The SDR has symbolic significance for the RMB because it contains the world’s “main” currencies. Additional fanfare comes from the RMB’s heavier weighting than the Japanese Yen and Pound Sterling.

| SDR Basket | Exchange Rate | Old Weight | New Weight |

|---|---|---|---|

| US Dollar | 1.0 | 41.9% | 41.73% |

| Euro | 1.0585 | 37.4% | 30.93% |

| Chinese Yuan | 6.3944 | 10.92% | |

| Japanese Yen | 122.67 | 9.4% | 8.33% |

| Pound Sterling | 1.5061 | 11.3% | 8.09% |

| SDR | 100.0% | 100.00% |

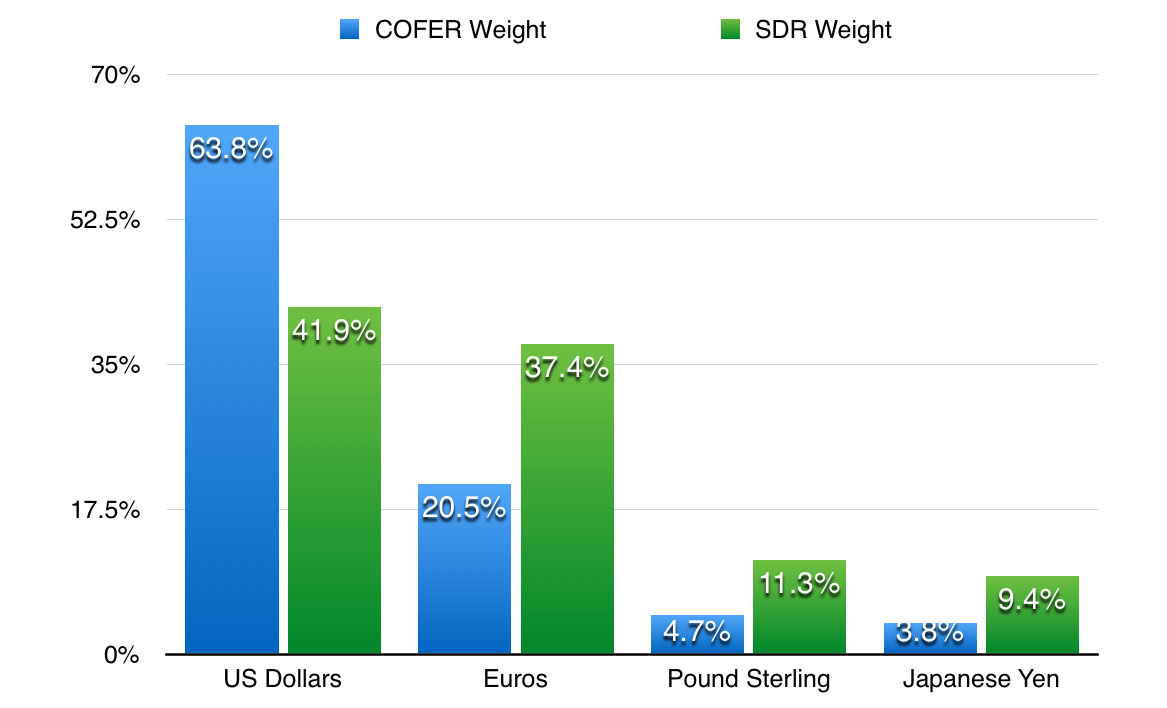

It is not true that central banks must replicate the composition of their foreign reserves based on the composition of the SDR basket. The below chart depicts the Composition of Official Foreign Exchange Reserves (COFER) to the composition of SDR based on data provided by the IMF in Q2 2015. Countries hold more assets in US dollar and less in other currencies than the SDR basket holds. The IMF states that countries are under no obligation to mirror their foreign reserves to the SDR basket. BAML estimates that IMF members may acquire up to US$35 billion of RMB to rebalance their SDRs, which is a negligible amount to affect yuan trading.

Andrew Colquhoun, head of Asia-Pacific sovereigns at Fitch: “What really matters is whether central banks and sovereign wealth funds start to see the renminbi as a viable store of liquidity and of value to rival the U.S. dollar. Such a shift seems unlikely while doubts persist over China's prospects for a smooth and orderly rebalancing, and while China retains widespread capital controls."